Key Trends and Trades from JPM Research 2025 Outlook

1/27/2025

Key Themes:

Higher Dispersion Across Markets: Expect increased variability across stocks, sectors, regions, and styles. This creates more opportunities for active management as equity leadership broadens.

US Exceptionalism with Turbulence: The US remains the global growth engine, supported by AI-driven investments, deregulation, and a healthy labor market. However, policy changes and geopolitical uncertainty could heighten volatility.

Uneven Global Growth: Resilient US expansion contrasts with structural challenges in Europe and emerging markets, where strong USD, high rates, and trade policy tensions weigh on growth. A sharp slowdown in China adds to global risks.

Geopolitical and Policy Complexity: Rising US-China tariffs, restrictive immigration policies, and potential election-driven shifts in fiscal and regulatory strategies add uncertainty to the global outlook.

Top Trades and Opportunities:

Equities:

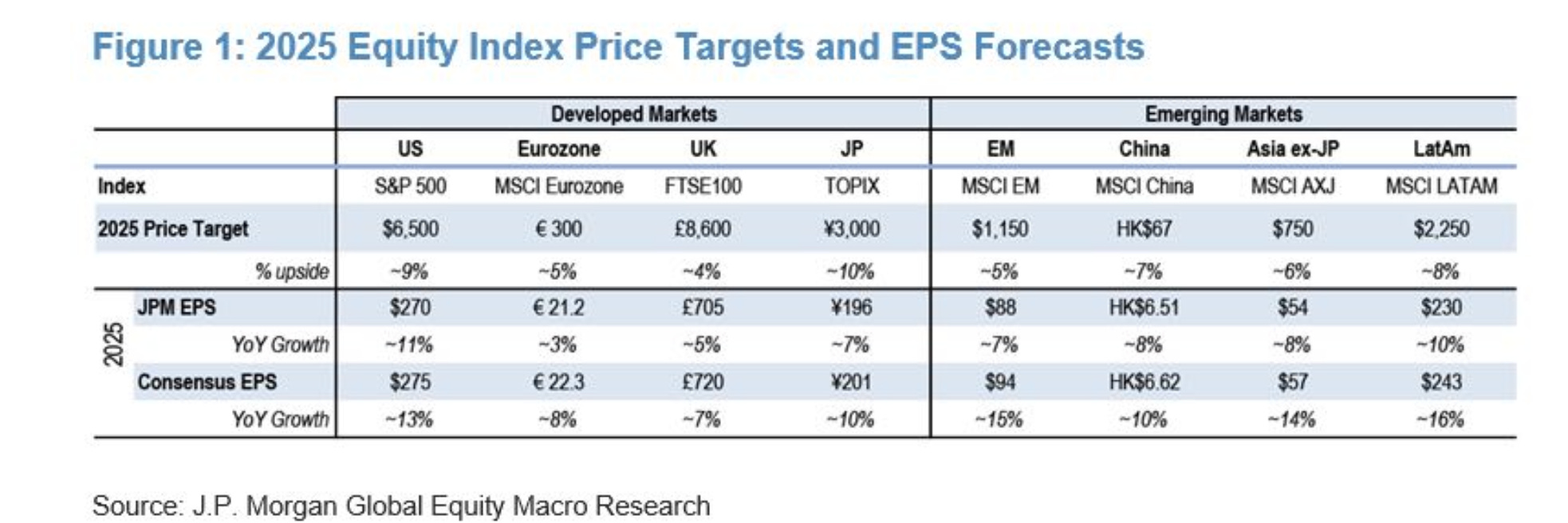

US Equities Favored: US markets remain the strongest play due to better fundamentals and a lack of quality alternatives in Europe or emerging markets. US Equities are the cleanest dirty shirt in the pile. DUBRAVKO’S 2025 SPX PRICE TARGET IS $6,500.

Potential Convergence Trade: Later in 2025, regional disparities could narrow if valuation and geopolitical clarity improve.

AI and Tech Investment: Broadening capital spending in AI and innovation sectors supports US productivity gains and capital markets.

Fixed Income:

Stay Long Front-End Treasuries: Favor lower yields in 2-year Treasuries due to dovish Fed bias and shallow rate-cutting cycles.

Steepening Trades: Position for 10s/30s steepeners but avoid broader steepeners exposed to rising term premiums.

Rate Outlook: Expect 100bps of easing by Q3 2025, with the Fed funds rate settling at 3.5%-3.75%.

FX:

USD Strength: The dollar is expected to hit new highs due to strong US growth, elevated rates, and productivity advantages.

G10 Carry Trades: Positive returns remain possible, but global carry trades will face challenges unless growth outside the US accelerates.

Key Themes: Watch for tariff risks (USD bullish), reliance on manufacturing, and policy divergence across regions.

Key Risks:

Policy Uncertainty: Election outcomes could trigger deregulation and fiscal boosts but also raise risks tied to tariffs, trade restrictions, and geopolitical retaliation.

Geopolitical Tensions: Higher US tariffs on China and reduced immigration across developed markets may trigger negative supply shocks, amplifying inflation and weighing on growth.

Global Divergences: Structural issues in Europe, uneven central bank actions, and weak emerging markets could widen regional disparities.

Sentiment and Supply Chain Risks: Aggressive US inward policies (e.g., trade curtailment, deportations) risk significant negative shocks to business sentiment and global supply chains. The global economy should experience a negative supply shock as US tariffs on China rise and as immigration is restricted across the DM. These impulses should raise inflation broadly and slow central bank easing.

Outlook Summary:

The global economy and equity markets are set for a dynamic 2025, with opportunities stemming from increased dispersion and US-led growth. Risks from policy shifts, geopolitical tensions, and uneven regional performance require a flexible and diversified approach to investing.