Summary Of Mike Nocerino’s GS Morning Rundown – February 7, 2025

Market Overview & Key Themes – Post-NFP Update: Jobs, Jitters, and AI Billions

U.S. futures were flat ahead of the Non-Farm Payrolls (NFP) report, with Goldman Sachs estimating +190K jobs(above the consensus of +175K). However, the actual print came in at a much lower 143K, missing expectations significantly. The unemployment rate, meanwhile, dropped to 4.0% from 4.1%, reflecting major revisions to labor force estimates.

So much for that +190K estimate—looks like Goldman overshot again. But thanks to upward revisions in prior months, the headline number isn’t as catastrophic as it seems.

Other economic data to watch includes Wholesale Inventories, Consumer Credit, and University of Michigan sentiment. President Trump is set to meet with Japan’s Prime Minister, with a press conference later today.

Looking ahead, next week is packed with major macro data, including CPI (2/12), PPI (2/13), and Retail Sales (2/14).

Market Movers – Adjusted for Jobs Data

Amazon (AMZN) -3%: Weak Q1 guidance despite strong AI-related CapEx spending.

Affirm (AFRM) +16%: Strong revenue and gross merchandise volume.

Expedia (EXPE) +10.5%: Positive revenue and outlook.

Bill.com (BILL) -28%: Lower revenue guidance.

Pinterest (PINS) +22%: Strong revenue outlook.

e.l.f. Beauty (ELF) -27%: Cut to full-year sales forecast.

CleanSpark (CLSK) +6.5%: Revenue beat.

Doximity (DOCS) +24%: Beat-and-raise earnings.

Take-Two Interactive (TTWO) +10%: Narrower loss and reiterated revenue guidance.

Skechers (SKX) -12%: Disappointing annual sales and profit outlook.

Fortinet (FTNT) +8.5%: Strong 2025 revenue forecast.

Focus: Non-Farm Payrolls & Economic Data

Goldman Sachs initially projected:

+190K jobs, above the +170K consensus.

Unemployment rate steady at 4.1%.

Hourly earnings rising 0.3% MoM, bringing YoY down to 3.7%.

Downward payroll revision of 818K jobs from April 2023 - March 2024, though they warned it could be misleading due to missing immigrant employment data.

New population controls potentially increasing labor force estimates.

What actually happened:

Payrolls came in at just +143K, well below estimates.

Unemployment rate dropped to 4.0% due to a 2.2M increase in the labor force from population adjustments.

Wages rose 4.1% YoY, stronger than expected.

Turns out the "strong" labor market is more of a statistical mirage—headline jobs missed, but massive revisions to past data and population adjustments conveniently clean up the mess.

Sector & Market Insights – Jobs Data Implications

Tech & AI:

Amazon is investing $100B+ in CapEx, primarily for AI infrastructure within AWS.

Chinese tech stocks rally after DeepSeek’s AI breakthrough, but Alibaba denies direct investment.

Tesla China deliveries fell 11.5% YoY, pressuring TSLA.

Commodities & Rates:

Oil prices drop as Trump’s tariff concerns outweigh Iran sanctions.

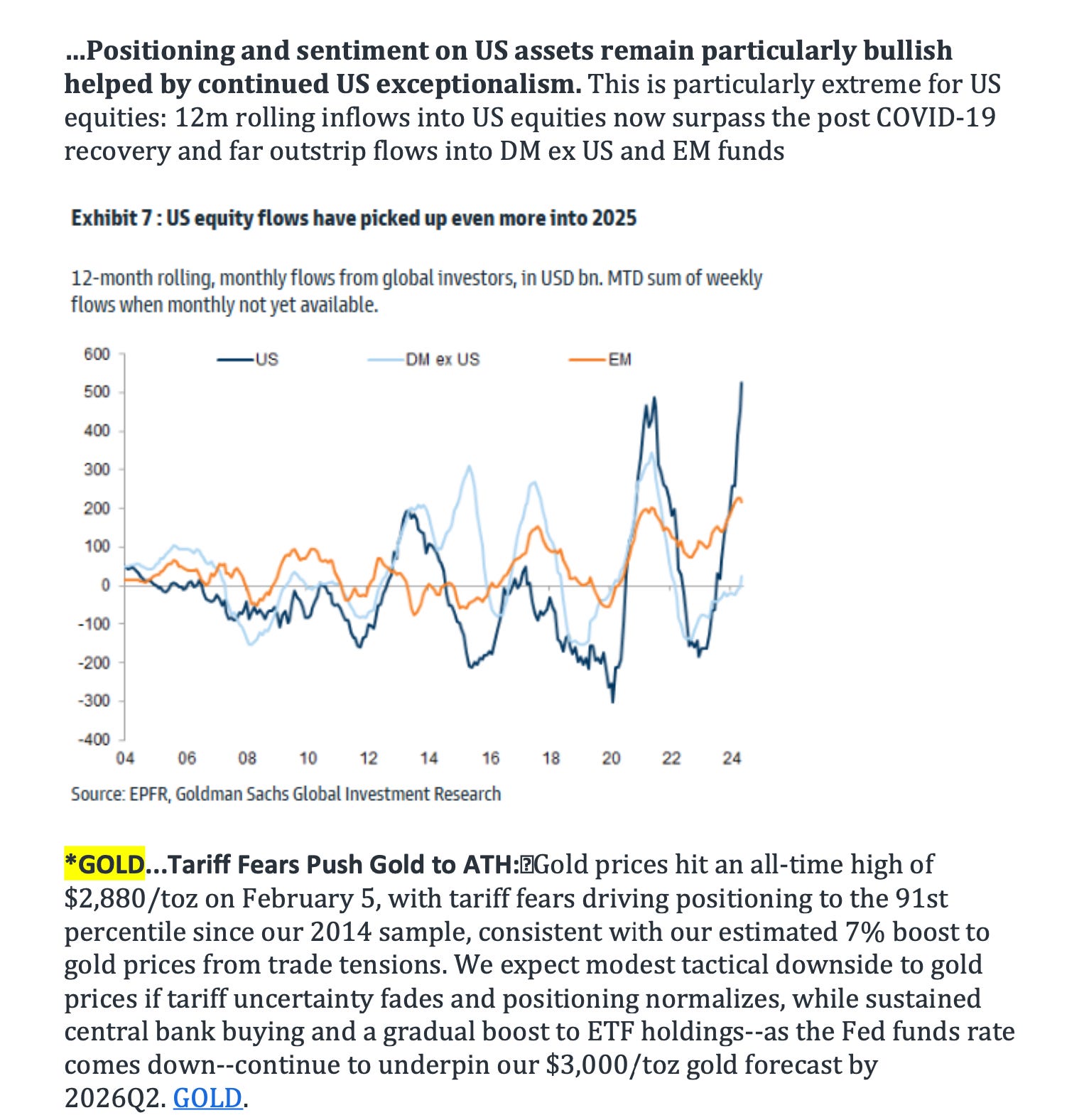

Gold hits an all-time high ($2,880/toz) on tariff fears, but GS sees potential downside if trade tensions ease.

If this NFP report spooks the Fed into rethinking rate cuts, gold’s rally might not be as smooth as expected.

Equity Positioning – Reassessing Post-Jobs Data

Goldman remains modestly pro-risk, overweighting equities and bonds, neutral on commodities/cash, and underweight credit. However, they flagged short-term equity correction risks due to stretched valuations and macro uncertainty.

With job growth slowing and wages running hot, the Fed will have a harder time justifying an aggressive rate-cut cycle. That could shake up the "AI-led bull run" thesis if markets start pricing in fewer cuts.

Stock Picks & Earnings Takeaways

Buy Recommendations (Unchanged):

Amazon (AMZN) & Pinterest (PINS): Strong Q4 earnings.

Fortinet (FTNT): Expected upside from cross-selling.

Business Development Companies (BDCs): Rising orders and margin expansion.

Philip Morris (PM): Solid beat-and-raise.

Tapestry (TPR): Strength in Coach brand.

Key Earnings Reactions:

e.l.f. Beauty (ELF) -26%: Cut guidance after a weak start to 2025.

Skechers (SKX) -12%: Missed expectations and lowered forecasts.

BYD +2%: Strong results continue to outperform auto peers.

General Motors (GM) & Ford (F): Under pressure from global supply chain risks and tariffs.

Final Thoughts – Post-NFP Market Positioning

Investor sentiment was bullish heading into 2025, but rising policy uncertainty and stretched equity valuations are raising caution flags. The focus remains on AI investment, macroeconomic trends, and sector-specific earnings surprises.

Weaker-than-expected job growth, rising wages, and massive revisions mean we’re in a "choose-your-own-adventure" macro environment. The bulls can point to a resilient labor force, while the bears highlight slowing momentum. Either way, expect volatility as markets digest the data and Fed rate-cut expectations shift.

Goldman Sachs still sees upside potential in equities but warns of short-term volatility, recommending hedges in gold, the dollar, and Treasury Inflation-Protected Securities (TIPS).